Emerging markets (EM) investments have been perceived, in some corners of the investor community, as inordinately high risk. We believe that perception is outdated. Emerging markets have evolved and, in many cases, have developed into mature and rapidly growing economic centres. With that evolution in EMs has come an increasing range of opportunities that are compatible with a variety of fund risk profiles and individual investor risk appetites. In this article, we challenge some of the lingering misconceptions about EM risk and illustrate, by virtue of our own experiences, how EM can be appealing to diverse, even conservative, investors who are inclined to see opportunities both for return and catalytic growth.

The evolution of emerging markets: today’s EM is no longer yesterday’s EM

Emerging markets are exactly that “emerging,” and have evolved significantly over time to the point where a “one size fits all” approach simply no longer applies. Countries throughout the developing world have become resilient to crises, weathering events such as the Latin American Debt Crisis of the 1980s and the Asian Financial Crisis of the late 1990s, only to come out stronger on the other side. Those events, and others similar, highlighted the need for robust economic policy and improved governance of EM financial systems. Many, if not most, EM countries have responded in kind, making critical investments in market infrastructure and regulation, and demonstrating for global investors a commitment to developing sophisticated markets, welcoming of foreign investment. The EM economies of 2024 are, in some critical respects, born of crisis and demonstrably able to endure them.

We have seen examples of countries such as India, Poland, and Brazil in which efforts to diversify the economy and establish sound regulatory and fiscal frameworks have led to remarkable growth. Each has demonstrated a clear understanding of the need to decrease reliance on single sectors, expand trade, and extract value from natural resources and domestic commodities in the global supply chain. Leveraging these opportunities during a period of global economic integration created pathways for these “Emerging Markets” to become powerful contributors to international trade and increasingly stable economies in their own right. Where we have seen the greatest potential is in those countries that have controlled public debt, implemented strong fiscal discipline as a matter of public policy, and made use of the international capital markets to raise debt strategically with a broad investor base. All these factors combined have led to an increasing number of attractive opportunities to participate in and support this growth within the boundaries of a still-cautious risk appetite.

Despite this broadly positive trend, not all EM stories have been positive. Certain countries rich in natural resources and recent history of prosperity have continued to see immense challenges and not shown a viable or consistent pathway to long-term stability. Argentina and Venezuela stand out as examples of this pattern. Both countries have grappled with hyperinflation, currency volatility, and an unstable position in the global economy due to recurring domestic governance and fiscal policy crises.

The new era: emerging markets have matured

As shown by the examples above, emerging markets are not, and should no longer be seen, as a single interdependent asset class. The individual markets and regions have evolved to the point where a single crisis in one EM does not have the same spillover effect it once did in others. In the past, a crisis in one country might have rippled across an entire region or an asset class, but as we have seen recently, this is not a foregone conclusion. The Russian invasion of Ukraine sent shockwaves through the global market in 2022, but EM corporate bonds have shown resilience and stability of credit quality, particularly and perhaps surprisingly in countries that have high dependencies on Russia.

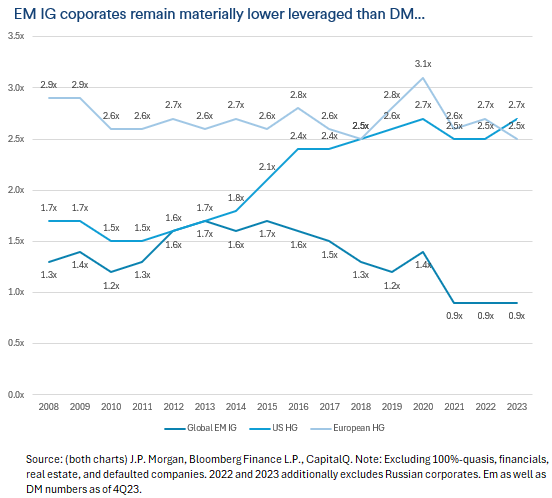

Shifting the lens from the macroeconomic landscape to the individual issuers within the EM corporate markets, we see a similar trend of growth and maturation. The asset class of EM corporate bonds has gained new traction among investors in recent years, which reflects the improved fundamentals, increased discipline, and resilience of issuers. This is true even in markets that are prone to disruption and crisis. We have observed, and research has shown, that the credit metrics of EM corporate bonds, as an asset class, have become increasingly comparable to, and in some cases superior to, those of issuers in developed markets. A prime example of this progress is the significant reduction in net leverage among EM corporate issuers, as indicated by JP Morgan research in a 2024 study.

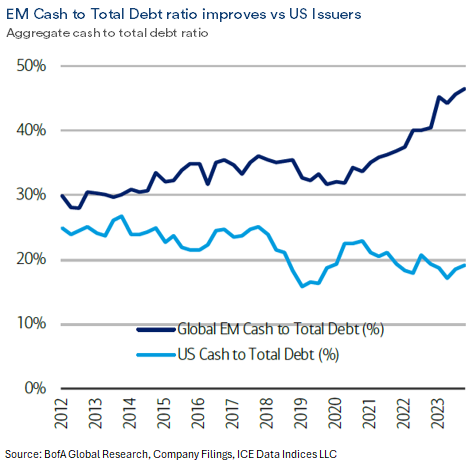

Despite having expanded access to local and international capital markets, EM corporates have managed to maintain relatively low leverage. This practice, on balance, has the tendency to leave issuers in a sound fiscal position and send a message to the global markets that those same issuers are disciplined in their approach to growth. To that point, the JP Morgan research referenced above shows a decrease of net leverage from a peak of 2.1x in 2016 to 1.2x in 2023. In the investment-grade space, EM corporates are materially less leveraged than their developed market counterparts; a trend that also extends to the category of high-yield EM corporates, albeit with a slightly narrower gap. Moreover, liquidity levels have significantly improved for EM corporates with cash to total debt hitting its all-time highs of above 45% (source: BofA Global Research). According to BofA Global Research, the gap between EM and US for the cash to total debt ratio has widened (EM: 46%; US: 19%).

Notwithstanding the relative discipline EM corporate issuers have shown in terms of leverage, the market for EM corporates has grown significantly. With many EM corporate issuers accessing capital markets, we have observed scale and diversity in the investment landscape that would have been hard to envision 10 or 20 years ago. That diversity of opportunity contributes to a diversity of risk profiles for investors in EM corporates, allowing conservative portfolio managers to focus on quality names with strong international ratings behind them. In our view, the opportunities are present and clear, but the key remains understanding the unique dynamics of EMs and investing with a well-informed strategy.

Improved credit quality in emerging markets

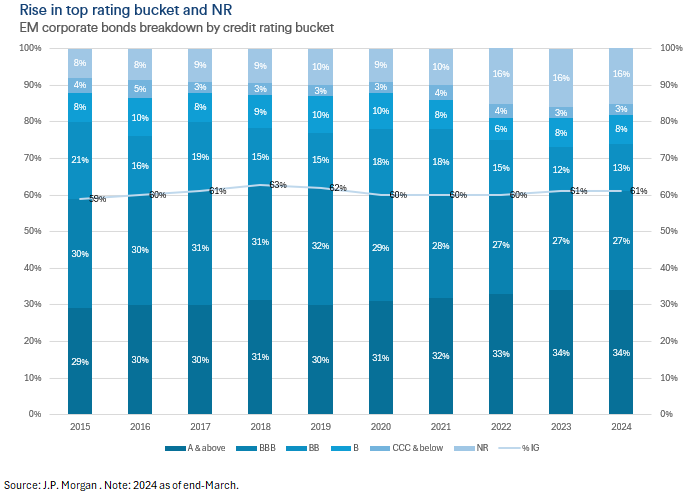

Emerging markets were once characterised by high growth potential accompanied by high risk. This assessment has changed and should continue to evolve from our perspective. According to JP Morgan Research, EM corporate bonds as an asset class have demonstrated significant improvement in credit quality, especially in top rating bucket. The higher rated single-A and above segment grew from 29% in 2015 to 34% in 2024. Conversely, the BBB and BB segments, which accounted for approximately 50% of the total in 2015, now make up only 40%. These indications are meaningful and reflect the broader trend we have observed in the maturation of corporate credit markets in the developing world.

Today, there are a number of examples of EMs that have undergone significant economic transformations and more closely resemble industrialised economies, in stark contrast to some EM perceptions. Markets such as Malaysia and Chile, supported by advanced economies, robust institutional frameworks, and sound economic policies, offer, in our experience, a wide range of high-quality credit opportunities. We view these markets not only as having good long-term potential, but as presenting strong and diversified class of issuers right now.

Active management & expertise: the key to navigating emerging markets

To embrace EM investing is to understand that, as an asset class, EM corporates present a wide range of opportunities. However, it is also crucial to acknowledge, and of equal importance, that there is no single “Emerging Market,” and each jurisdiction is and will remain unique. The idiosyncratic risk return profile of EM investments drives the need for active management and expertise. We see regular opportunities to take advantage of dislocations in discrete emerging markets and select value opportunities where others see excessive risk. This approach derives from experience and understanding of the political, economic, and monetary policy factors, to name a few, that drive trends in various EMs. The disparities in performance from one EM to another, at any given time, underscore the complexity of EMs. They also highlight the need for active management of a kind that derives from deep understanding of specific markets and an on-the-ground presence to separate fact from fiction in pursuit of issuer selection and alpha generation.

Key take-aways

The bottom line is that emerging markets are no longer a monolith. They have matured almost across the board and offer investors a broad range of diversified investment opportunities in the corporate debt asset class. EMs are defying assumptions across continents and generating alpha for investors willing to look beyond preconceptions and look closely at the steady and maturation and improvement of EM credit quality. It is not exaggeration to suggest that some EM corporate issuers possess fundamentals equal to or better than investment-grade issuers in developed markets. You simply must know where to look and understand what elements of an emerging market economy could impact those fundamentals. This is, in effect, no different than the approach to portfolio selection in development market corporates. It simply requires different expertise. Even in spite of all the challenges in today’s geopolitical environment, we remain confident that the continued growth of EMs and the sound foundations many issuers have built in the past decade will present attractive opportunities in debt markets for a long time to come.

-end-

Important Information

This document was produced by BlueOrchard Finance Ltd (“BOF”) to the best of its present knowledge and belief. Information herein is believed to be reliable, but BOF does not warrant its completeness or accuracy. BOF has expressed its own views and opinions in this document, and these may change. They do not necessarily reflect the opinion of Schroders Group.

BOF is part of Schroders Capital, the private markets investment division of Schroders Group.

This information is a marketing communication and is not to be seen as investment research. As such it is not prepared pursuant legal requirements established for the promotion of independent investment research nor subject to any prohibition on dealing ahead of the distribution of investment research.

The information in this document is the sole property of BOF unless otherwise noted and may not be reproduced in full or in part without the express prior written consent of BOF.

Any reference to sectors/countries/stocks/securities are for illustrative purposes only and not a recommendation to buy or sell any financial instrument/securities or adopt any investment strategy.

All investments involve risks. Past performance is not a guide to future performance and may not be repeated. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. Exchange rate changes may cause the value of investments to fall as well as rise. Performance data does not take into account any commissions and costs, if any, charged when units or shares of the fund are issued and redeemed.

Emerging markets impact investments involve a unique and substantial level of risk that is critical to understand before engaging in any prospective relationship with BOF and its various managed funds. Investments in emerging markets, particularly those involving foreign currencies, may present significant additional risk and in all cases the risks implicated in this disclaimer include the risk of loss of invested capital. To understand specific risks of an investment, please refer to the currently valid legal investment documentation.

This document may contain “forward-looking” information, such as forecasts or projections. Please note that any such information is not a guarantee of any future performance and there is no assurance that any forecast or projection will be realised. Scenarios presented are an estimate of future performance based on evidence from the past on how the value of this investment varies, and/or current market conditions and are not an exact indicator. BOF does not in any way ascertain that the statements concerning future developments will be correct. Unless this fund contains a capital guarantee, what you will get will vary depending on how the market performs and how long you keep the investment/product. Performance is subject to your individual taxation circumstances which may change in the future.

This document does not constitute an offer to anyone, or a solicitation by anyone, to subscribe for shares of a fund managed or advised by BOF. Nothing in this document should be construed as advice and is therefore not a recommendation to buy or sell shares. An investment in a fund entails risks, which are fully described in the fund’s legal documents.

We note in particular that none of the investment products referred to in this document constitute securities registered under the Securities Act of 1933 (of the United States of America) and BOF and its managed/advised funds are materially limited in their capacity to sell any financial products of any kind in the United States. No investment product referenced in this document may be publicly offered for sale in the United States and nothing in this document shall be construed under any circumstances as a solicitation of a US Person (as defined in applicable law/regulation) to purchase any BOF investment product.

The material is not intended to provide, and should not be relied on for, accounting, legal or tax advice, or investment recommendations.

By no means is the information provided in this document aimed at persons who are residents of any country where the product mentioned herein is not registered or approved for sale or marketing or in which dissemination of such information is not permitted. Persons who are not qualified to obtain such document are kindly requested to discard it or return it to the sender.

No Schroders entity nor BOF accept any liability for any error or omission in this material or for any resulting loss or damage (whether direct, indirect, consequential or otherwise), in each case save to the extent such liability cannot be excluded under applicable laws.

The BlueOrchard managed funds have the objective of sustainable investment within the meaning of Article 9 Regulation (EU) 2019/2088 on Sustainability related Disclosure in the Financial Services Sector (the SFDR). For information on sustainability related aspects of this fund please go to https://www.blueorchard.com/sustainability-disclosure-documents/ .

The fund’s prospectus, key investor information if any and annual reports are available free of charge upon request at BlueOrchard Asset Management (Luxembourg) S.A., 1 rue Goethe, L-1637 Luxembourg. The prospectus and the Key Investor Information for Switzerland, if any, the articles, the interim and annual reports, the list of purchases and sales and other information can be obtained free of charge from the representative in Switzerland: 1741 Fund Solutions AG, Burggraben 16, 9000 St. Gallen. The paying agent in Switzerland is Bank Tellco AG, Bahnhofstrasse 4, 6430 Schwyz.

BOF may decide to cease the distribution of any fund(s) in any EEA country at any time but we will publish our intention to do so on our website, in line with applicable regulatory requirements.

Third party data is owned or licensed by the data provider and may not be reproduced or extracted and used for any other purpose without the data provider’s consent. Third party data is provided without any warranties of any kind. The data provider and issuer of the document shall have no liability in connection with the third-party data. The Prospectus contains additional disclaimers which apply to the third-party data.

Source: MSCI

MSCI makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indexes or any securities or financial products. This report is not approved, endorsed, reviewed or produced by MSCI. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

BOF has outsourced the provision of IT services (operation of data centers, data storage, etc.) to Schroders group companies in Switzerland and abroad. A sub-delegation to third parties including cloud-computing service providers is possible. The regulatory bodies and the audit company took notice of the outsourcing and the data protection and regulatory requirements are observed.

A summary of investor rights may be obtained from https://www.blueorchard.com/imprint/

Copyright © 2024, BlueOrchard Finance Ltd. All rights reserved.